马尼托巴养猪研讨会:行业仍有较大空间可改进(2)

- 点击次数:

- 日期:2013-02-17 18:00

- 编辑:admin

- 来源:加裕周评

- 评论

我们发现了一个很有趣的现象。PIC的Melody先生的大量数据表明,在过去三年间断奶至育肥利润前25%的生产者,188日龄达272公斤、料肉比2.69、死亡率7.7%。这让我们很惊讶。因为来自PIC的Melody先生所展示的这些数据与我们听到的行业前25%的结果比起来相当差。我们经常听到生产者声称2.3的饲料转化率(包括种猪公司)。很难相信比最好的25%还要好0.4?同时他们宣称断奶至育种死亡率为4%,而前25%为7.7%。188天上市意味着有一半的生产者超过188天。这并不突然,真实的行业仍有大量空间可以改进。

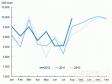

2012年损益帐

艾奥瓦州立大学计算了分娩至育肥场的月度及年度损益情况。

十二月的损益情况为每磅活重损失73.96美分,每头损失31.54美元。十二月的损益情况为每磅活重损失68.16美分,每头损失12.47美元。

亏损总是不好的。十二月每头亏损31.53美元乘于这个月的1000万头商品猪,等于整个行业亏损3亿美元。

我们的养猪者全年每头亏损12.47美元乘于1亿2000万头商品猪,将导致全行业14亿美元的亏损。

巨大的亏损。这个情况并不好。我们仍然非常难相信,美国农业部12月1日的生猪报告表明美国母猪存栏出现扩张的情况。如果这样的话,我们真的是有快速恢复的行业以及非常乐观的银行家。很难相信在现金亏损的情况下还会有扩张的行为。

原文:

PorkCommentary Feb 4, 2013 – Cattle Supply Plummets

时间: [ 2013-02-04 18:05 ]

Cattle Supply Plummets

The US Hog industry should get a significant boost from the lack of cattle.

• January 1st Cattle Inventory 2013 89.3 million head – 2 per cent lower or 1.5 million head fewer than January 1st 2012 (90.8 Million).

• The lowest January 1st Cattle Inventory since 1952

• All cows and heifers January 1st 2013 were 38.5 million down 900,000 from last years. 39.4 million on January 1st.

• The lowest Cow and Heifer inventory since 1941!

The lowest cattle number in 60 years! The lowest cow and heifer numbers in 70 years! The beef supply continues to plummet with no sign of stabilizing. Less Beef is always positive for Pork Prices. We are the only Red Meat Option.

Wean to Finish Data

Last week we attended the Manitoba Swine Seminars. One of the speakers was Brian Melody PIC Wean –Finish Technical Service Manager, Ames Iowa. Mr. Melody gave a very informative talk. What we found interesting is the actual results he presented on Wean-Finish data.

Database Summary Comparison of Average and High Profit Producers (2010-2012), Brian Melody, PIC

We have to say we found it very interesting that PIC’s Mr. Melody’s massive database indicated that the top 25% producers based on profit had wean to finish results over the last three years of 188 days to 272 lbs. and a feed conversion of 2.69 with mortality of 7.7%. What surprises us is how poor these numbers are that Mr. Melody from Pic presented relative to the what we hear the industry believes top 25% results are. We hear often producers claiming 2.3 feed conversions (also genetic companies). Hard to believe .4 better than the top 25%? Also mortality wean to finish claims of 4% when top 25% – 7.7% 188 days to market means half of all producers are over 188 days. Not very spectacular. Lots of room for real industry improvement.

2012 Profit and Loss

Iowa’s State University calculates break-evens monthly and yearly for farrow to finish operations.

December Break-even 73.96 ₵/lb. liveweight loss per head $31.54 2012 Annual Break-even 68.16 ₵/lb liveweight loss per head $12.47.

Losing money isn’t good. $31.54 per head December times 10 million market hogs for the month would equal $300 million loss for the industry.

Annual our farmer arithmetic $12.47 per head loss times 120 million market hogs produced would be about $1.4 billion industry losses.

Big loss. Not a good scenario. We continually have a real hard time believing the USDA December 1st Hog & Pigs Report that shows the US sow inventory had expanded. If so we truly have a very resilient industry and very optimistic bankers as it’s hard to believe expansion coming from a negative cash flow.

- 2013-02-18研究表明生猪患痢疾的元凶或是螺菌属微生物

- 2013-02-15河南畜牧产业化(生猪)集群襄城实验区正式投产

- 2013-02-08欧盟批准从美国进口生猪 从2月25日起生效

- 2013-02-06加拿大猪肉研讨会认为媒体应当促进消费者与生产者之间的联系

- 2013-01-292012年美国生猪报价与同期相比总体保持平稳

- 2013-01-28美国中西部猪农将面临更重的赋税

- 2013-01-25美国强制性标签政策让加拿大生猪行业损失严重

- 2013-01-25班夫养猪研讨会

- 2013-01-24加拿大西部的养猪业重组

- 2013-01-22荷兰应用DNA技术检测和治疗生猪疾病

| 查看所有评论 最新评论 | |

|

|

|

| 发表评论 | ||||

|

- 欧盟仍有17国未能完全执行母猪限位栏 255

- 报告显示英国去年抗生素使用量大幅下滑 237

- 拉脱维亚爆发五起非洲猪瘟疫情 223

- 河南畜牧产业化(生猪)集群襄城实验区 219

- 欧盟批准从美国进口生猪 从2月25日 213

- 发现莱克多巴胺,俄将禁止美国牛肉和猪 212

- 加拿大猪肉研讨会认为媒体应当促进消费 208

- 美国本月的猪肉以及牛肉出口同此下滑 207

- 寒冷天气阻碍俄罗斯境内非洲猪瘟疫情的 200

- 荷兰应用DNA技术检测和治疗生猪疾病 196